Overall Risk-Taking Score

|

|

We monitor the backdrop for investing in risk assets across three primary pillars: economic conditions, asset prices, and technical considerations such as investor sentiment and price momentum. Since last month, our assessment of the environment for accepting investment risk declined by one degree to neutral. The primary drivers of this change is household sentiment, which has risen above long-term averages, and the robustness of technical metrics declining modestly.

The change in overall risk-taking score month-over-month is the result of modestly lower scores, though many elements of the overall risk-taking score remain healthy. For example, household sentiment remains in an uptrend and has yet to approach overly exuberant levels, though the decline in this scoring input into the overall model is an acknowledgement that it now has less room to improve than it did in the previous month.

The economy remains healthy on average; households are in good financial shape, seeing wage gains, and spending. The labor market is improving, and financial conditions are quite accommodative. Risk asset classes such as equities and credit are trading above long-term averages, which is the primary factor holding back the overall risk-taking score. The potential for an extended period of above-average inflation also gives us pause. Given current conditions, we advocate investors:

- Trim exposure to risk assets such as equity and credit back to target weights after rallies.

- Position toward higher quality companies with less-cyclical revenue and earnings.

- Add strategies that may be less sensitive to above-average inflation or even profit from it.

- Add alternative strategies that are less correlated to traditional stock and bond markets.

- Favor actively managed funds as these tend to add the most value during inflection points in the market relative to their index-based counterparts.

Economy

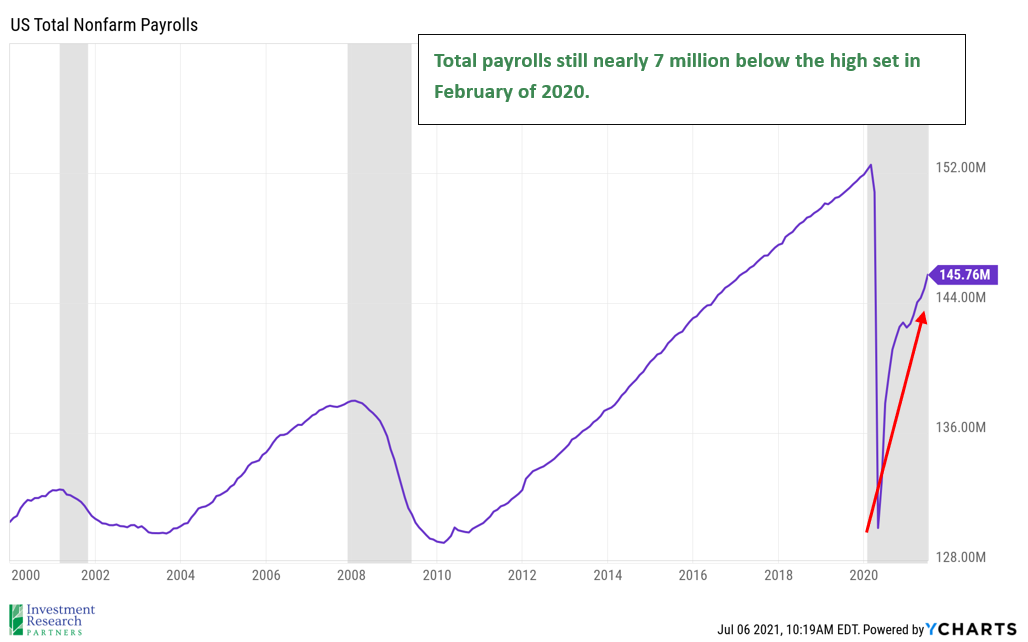

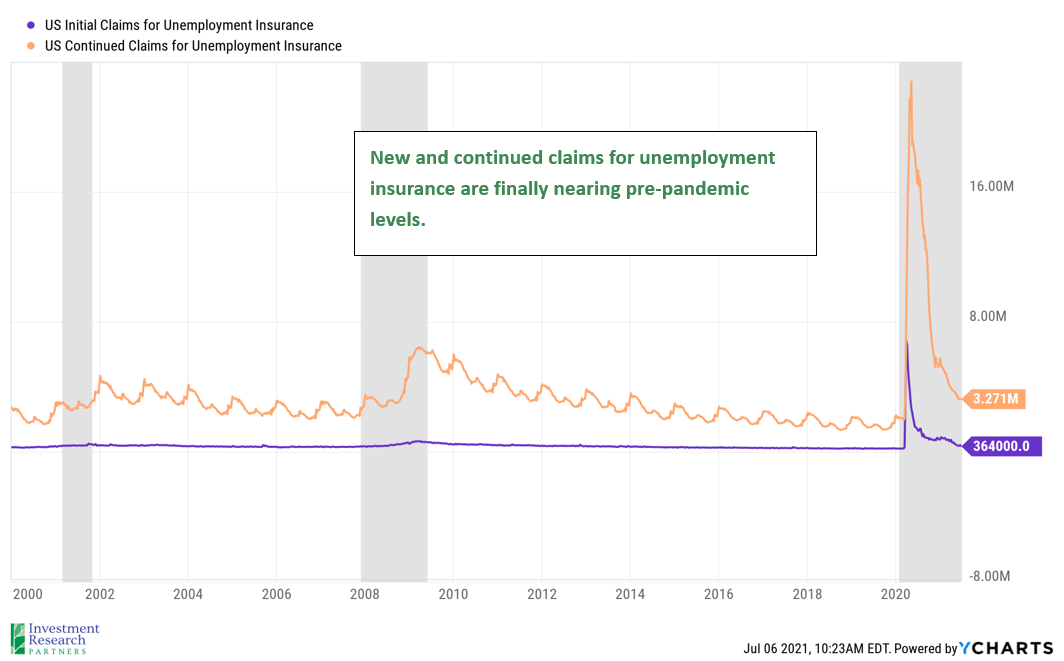

The labor market continues to improve. Last Friday, the Bureau of Labor Statistics reported that US payrolls rose 850,000 in June to nearly 146 million. Despite the increase in the number of employed Americans, the headline unemployment rate actually rose to 5.9% from 5.8% in May as more individuals entered the labor force. Following a similar theme to the previous months of 2021, leisure and hospitality saw the largest gain in employment (+343,000 jobs) as restaurants, hotels, and travel all continue to return to pre-pandemic levels.

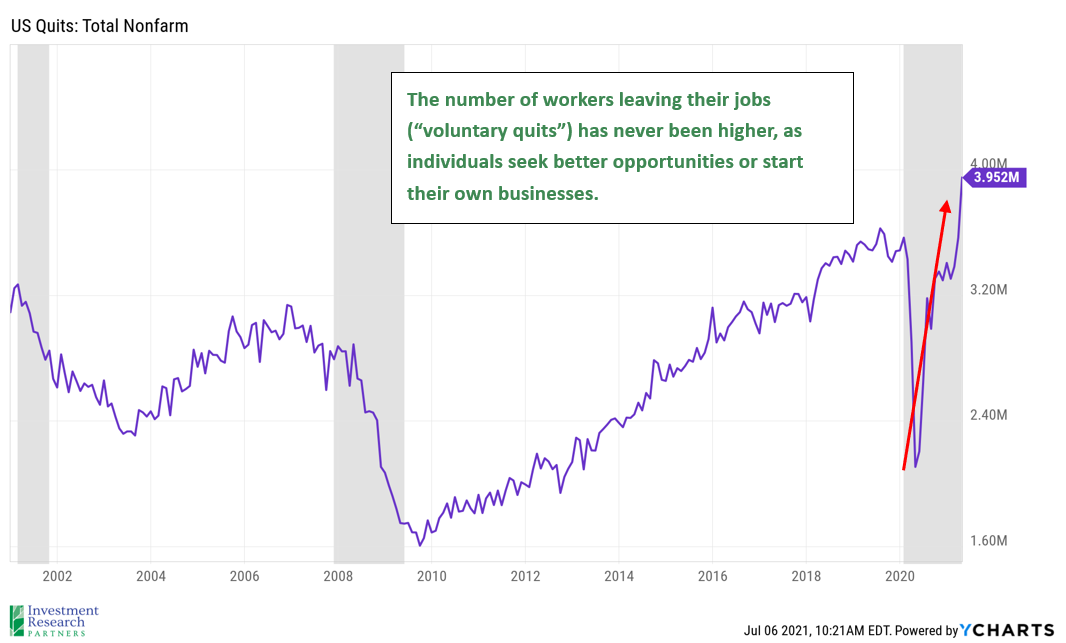

Encouragingly, the labor market has room for continued improvement, with total nonfarm payrolls still nearly 7 million below the high of February 2020. This implies that the economy has continued capacity for growth and improvement before traditional late-cycle wage pressures begin to challenge profitability. Of course, the confluence of factors such as abrupt economic shut-downs and re-openings as well as unprecedented stimulus have made this recession and recovery unique. Wage pressure and the availability of workers have already begun to challenge certain industries. Additionally, the number of workers leaving their jobs for better opportunities is now at an all-time high.

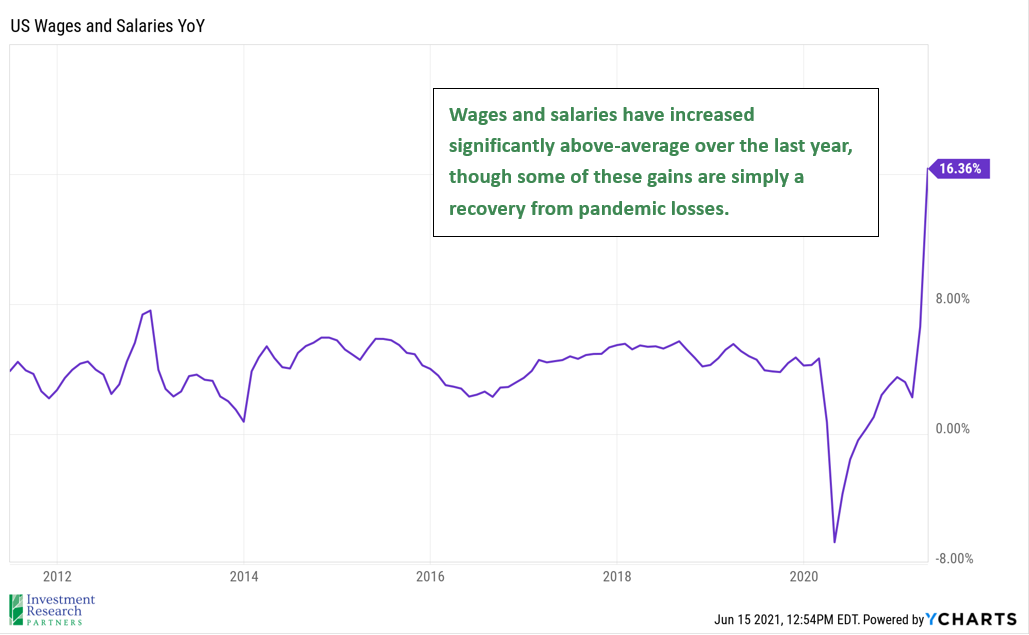

Inflation, or the potential for higher prices for goods, services, and assets, has become a concern for investors in 2021. For the last 10 years, the accommodative monetary policy from the US Federal Reserve and central banks globally has pushed the prices of assets such as stocks, bonds, and homes higher. This is potentially a positive form of inflation for those fortunate enough to own these instruments. For example, the average existing home sales price increased 117% since the start of the century, and the S&P 500 has returned 342%, despite three US recessions in the last 20 years.

Should you be worried about inflation? Click here to find out.

However, traditional measures of inflation, such as the Consumer Price Index published by the Bureau of Labor Statistics, focus on costs of living such as food & beverages, housing, medical care, transportation and education. Since the start of the century, consumer prices are 60% higher, with roughly 4.4% of that increase occurring in the last year ending June 30th. While the sharp increase in costs of living over the last year can be painful for those who do not own financial assets or who are on a fixed income, we believe that the current wave of higher costs will subside and trend toward normal levels. We expect that supply and demand for goods and services will find a natural balance over the next 12 months as more supply comes back online and demand from consumers moderates in the face of higher prices.

Corporate Earnings

Earnings season is upon us, and the consensus estimate of analysts surveyed by Factset is for 64% year-over-year earnings growth for the second quarter of 2021. Of course, this year-over-year growth rate is significantly above average largely due to the wash-out in corporate earnings that was experienced in the second quarter of 2020 (the depth of the pandemic lock-downs).

Valuation

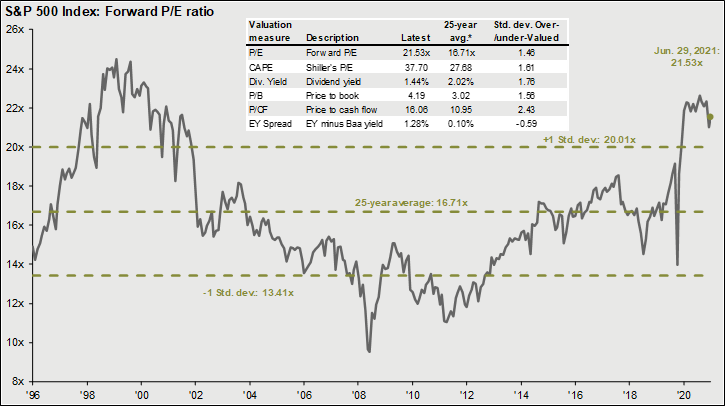

The prices for risk asset classes such as equity and credit are above long-term averages, and this input is primarily responsible for holding back our overall risk-taking score (see above). The chart below highlights the price investors are willing to pay for expected future earnings of the S&P 500 index (“forward price-to-earnings ratio”). This same relationship is true to varying degrees for most asset classes today. Encouragingly, the increase in reported and expected earnings have helped to push the S&P 500 index’s valuation back toward a range of normalcy over the last few months.

Source: Barclays, Bloomberg, FactSet, Standard & Poor’s, Thomson Reuters, J.P. Morgan Asset Management.

Price-to-earnings is price divided by consensus analyst estimates of earnings per share for the next 12 months as provided by IBES since February 1996, and J.P. Morgan Asset Management for April 30, 2021.

Guide to the Markets – U.S. Data are as of June 29, 2021.

Asset Class Returns

| Category | Representative Index | June 2021 | YTD 2021 | Full Year 2020 |

|---|---|---|---|---|

| Global Equity | MSCI All-Country | 1.4% | 12.3% | 16.3% |

| US Large Cap Equity | S&P 500 | 2.3% | 15.3% | 18.4% |

| US Small Cap Equity | Russell 2000 | 1.9% | 17.5% | 20.0% |

| Foreign Developed Equity | MSCI EAFE | -1.4% | 8.8% | 7.8% |

| Emerging Market Equity | MSCI Emerging Markets | 1.3% | 7.5% | 18.3% |

| US High Yield Fixed Income | ICE BofAML High Yield Bond | 1.4% | 3.7% | 6.2% |

| US Fixed Income | Barclays Aggregate Bond | 0.7% | -1.6% | 7.5% |

| Cash Equivalents | ICE BofAML 3 Mo Deposit | 0.0% | 0.0% | 0.5% |

| Source: Morningstar (total returns shown gross of fees) As of June 30, 2021 |

Prices & Interest Rates

| Representative Index | June 30, 2021 | Year-End 2020 |

|---|---|---|

| S&P 500 | 4,298 | 3,756 |

| Dow Jones Industrial Avg. | 34,503 | 30,606 |

| NASDAQ | 14,504 | 12,888 |

| Crude Oil (US WTI) | $73.47 | $48.42 |

| Gold | $1,771 | $1,902 |

| US Dollar | 92.44 | 89.94 |

| 2 Year Treasury | 0.25% | 0.13% |

| 10 Year Treasury | 1.45% | 0.93% |

| 30 Year Treasury | 2.06% | 1.65% |

| Source: Bloomberg, US Treasury (total returns shown gross of fees) As of June 30, 2021 |

Download PDF Version